Last night I wasted Field of Dreams with the kids. Plenty of complaints before the start. One wanted to watch Avengers, another didn’t want to watch a sports movie. The other one was opposed to the entire endeavor.

They came around pretty quick. But here was my big takeaway: I’m on the verge of becoming a naturalized citizen in the commodity world--I couldn’t stop thinking about how all the farmers were appalled and outraged when Kevin Costner dug up his corn to build the baseball field. And then there was the clearly disastrous financial implications, where this decision put his farm on the verge of bankruptcy.

I had questions. 1) how much corn did he dig up? 2) how much revenue did he forego, in absolute terms and relative to the size of the farm? 3) Given a few assumptions, was this really a farm-wrecking decision, or was this Hollywood stuff?

In 1987 many farms in Iowa were between 250-500 acres, and this same data shows a husband/wife team could have eked out a living managing such farm. Let's assume this was a 250 acre farm.

The average value per acre in Iowa was $875 in 1987, around the depth of the US farm crisis. A 250-acre farm could have been had for around $220,000. Lets call it $280k with a modest farm house on the property. Putting say, $60k down on such a property was certainly within reach for a college educated, dual income couple in their mid-30s that has been working and saving for 10-15 years.

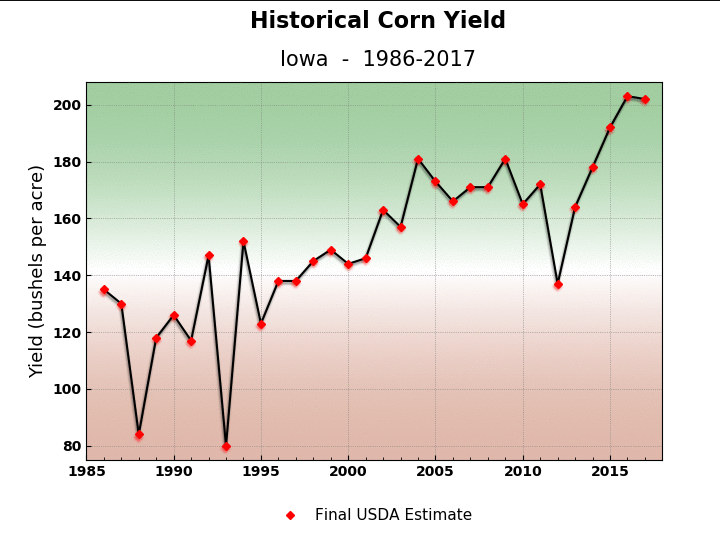

The average farm price for corn in 1987 was $1.89/bushel. And one might expect an acre of corn to yield around 120 bushels of corn.

So 250 acres of corn, yielding 120 bushels nets you 30,000 bushels of corn. Lets say Kevin Costner is a particularly crafty basis trader and he gets $2/bushel for his corn. He grosses $60,000. The 1987 census report above suggests such a farm might generate $20-$30k in net income--enough to live on if you’re into the lifestyle--but there were many farms during that time that were losing money. Bankruptcy was certainly on the mind of every US farmer in the mid-late 80s.

But with foul territory and some residual space for bleachers, you’re probably looking at another acre. But no more than 4.5 acres total, even if you add in a few parking spaces.

Let's say Kevin Costner dug up four acres of corn. That’s less than $1000 in foregone revenue in the year he dug it up (it probably had some residual silage value!) and in the new crop year when Shoeless Joe finally showed up.

So our hero gave up $1000 out of $60,000 in revenue, and maybe $30,000 in net income. Let’s add on another $1000 for the infield dirt, the grass he planted, and the backstop fence. Despite the gossiping and murmuring of the other farmers and their wives, he certainly could have billed it as a community service--and heck, even written it off on his taxes--since presumably he didn’t just let the field sit there..he let the local farm-kid teams play on it while he was waiting for whatever was supposed to happen.

An aggressive financial decision, but one easily justified by hearing a voice say, “If you build it, he will come.”

Kevin Costner made one crazy, totally unjustifiable decision: he lit the field!!

This, is what would have bankrupted his farm. This is the decision that would have had his smarmy brother-in-law questioning his sanity. Lighting the field today would easily get you into six digits, and would certainly have been out of reach for a financially strapped family farmer in the midst of an agricultural crisis.

Sure, it made for the coolest scene in the movie.

But completely implausible.

Here’s a few light-hearted takeaways for market analysis:

Question assumptions. We all have a cognitive bias to buy into what we’re being told. It’s called “Truth Default Theory”. It’s what makes movies work….but it often turns into a trap in markets.

Sometimes the trade is not where you think. Everyone jumped on Kevin Costner for digging up his corn--but it was the lights that were financially reckless.

Everyone loves a story. Many trades are long on “story” because stories sell. You’re not going to get your boss to buy into upsizing your trade because of your spreadsheet. You need a story.

But….every story needs data. Stories without data are just that, Hollywood stories. A good story combined with solid data can go a long way.

But most important:

Be open to changing your mind. I didn’t mention this above, but the key point of the movie is when the fussy pants brother-in-law has his epiphany. This was a man that was deep into his own trade to buy Kevin’s farm. But he changed his mind. That this was done only with divine intervention is irrelevant! Too often we get wedded to ideas and refuse to accept the metal cost of accepting that we were wrong and changing course.

Love your ideas, but don’t be afraid to set them free.